Mergers and acquisitions (M&A) have surged in the Trust and Corporate Service Provider (TCSP) and wealth management sectors, driven by a need for scale and efficiency in a highly fragmented industry[1][2]. Shareholders – from private equity investors to CEOs – are keenly focused on how post-merger investments translate into EBITDA growth. Common post-deal plays include expanding into new geographies, broadening product/service offerings, growing the workforce, and – increasingly – investing in digital transformation. Yet research shows that nearly 68% of acquisitions fail to meet their expected value creation targets, often due to integration challenges[3]. This article examines current insights on why digital integration after M&A is emerging as a superior value driver, especially in TCSP and wealth management, and how its EBITDA impact compares to more traditional integration strategies.

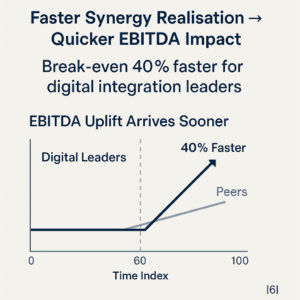

Post-merger digital transformation – integrating IT systems, automating processes, harmonising data, and leveraging AI – is now viewed as a critical lever for value creation. In fact, 87% of business leaders in a recent survey rated a target’s digital integration capability as “critical” or “very important” when evaluating acquisitions[4]. The rationale is clear: effective digital integration accelerates synergy realisation and boosts profitability. A McKinsey study finds that companies excelling at digital post-merger integration achieve on average 32% higher synergy benefits within 24 months of acquisition[5]. These “digital synergy” leaders also reach break-even 40% faster and face a 65% lower probability of major integration issues[6][7]. In other words, digital maturity directly correlates with stronger and quicker EBITDA contribution after a deal.

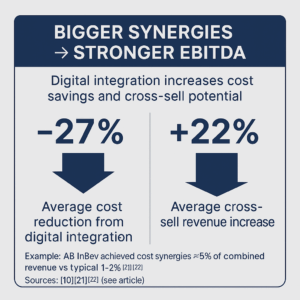

For TCSP and wealth management firms, the appeal of digital investment is especially strong. These businesses often accumulate siloed legacy platforms across jurisdictions and functions – a typical mid-sized firm might operate 14 different core applications with minimal integration[8]. M&A only amplifies this IT patchwork. Consolidating such disparate systems is costly (IT integration can consume ~40% of total PMI costs[9]), but it offers enormous upside: consolidating data centres and infrastructure yields 20–35% savings in ongoing IT operating costs[9]. Digitally unifying workflows (client onboarding, compliance, portfolio management, etc.) can unlock both cost efficiencies and new revenue streams. A PwC analysis of 217 transactions in 2023–2025 quantified the gains from post-merger digital excellence: revenue synergies up 14–22% via cross-selling enabled by integrated customer data, cost synergies of 18–27% through IT consolidation, and 30–40% faster process cycle times thanks to automation[10]. Such improvements directly boost EBITDA margins – by cutting redundant costs and by driving additional fee income without commensurate expense growth.

Crucially, digital transformation is not just about IT – it’s about integrating people and processes along with technology. Effective integration of disparate systems and workflows creates a more scalable operating model for the combined firm. For example, in wealth management M&A, unifying client data into one CRM and analytics platform enables advisors to identify cross-selling opportunities (increasing revenue per client) while streamlining reporting and compliance (reducing labour costs). In TCSP businesses (which handle entity administration, trust accounting, and regulatory filings), automating manual compliance tasks and consolidating multiple jurisdictional systems can sharply reduce overhead as well as reduce risk. It’s telling that private equity-backed platforms are actively investing in digitising the TCSP industry – for instance, in 2024 Quantios acquired Klea, an AI-powered legal entity management tool, to integrate into a TCSP software provider and automate core corporate administration workflows[11]. The expectation is that such post-merger digital upgrades will translate into improved EBITDA through efficiency and better client service capacity.

![]()

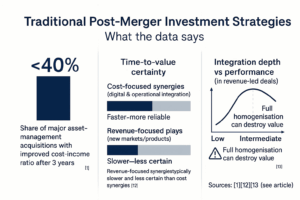

Aside from technology, acquirers often pursue more traditional post-merger integration strategies: expanding the combined firm’s geographic footprint, diversifying its products or services, or beefing up the workforce. These approaches can indeed drive growth, but their impact on EBITDA tends to be less immediate and more variable compared to digital optimisation:

Research and experience indicate that cost-focused synergies (often achieved through digital and operational integration) tend to deliver value faster and more reliably than revenue-focused plays like new markets or products[12]. In successful deals, acquirers align the integration approach to the deal’s value thesis: if the goal is efficiency and cost reduction, deep integration (consolidating systems, centralising functions) drives EBITDA improvement; if the goal is revenue growth, a lighter integration touch may preserve the innovative or market-specific advantages of the target[13]. Getting this balance right is crucial. Traditional strategies such as expansion and diversification do contribute to growth, but digital integration has emerged as the connective tissue that can amplify their success – or conversely, if neglected, can undermine these strategies through operational inefficiency.

No matter the strategy, the integration process itself is often the single biggest challenge in post-merger value creation. Bringing together two companies’ systems, workflows, and cultures is a complex undertaking – but also a huge opportunity if done right. In TCSP and wealth management deals, integration issues loom large: firms must reconcile different IT platforms (portfolio management systems, client databases, compliance tools), different operating procedures, and entire teams of people used to working a certain way.

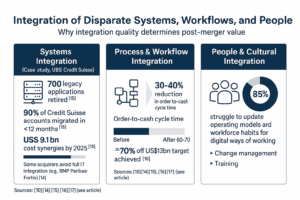

Systems Integration: Technology integration is frequently the linchpin of post-merger success in these sectors. Merging banks, wealth managers or corporate service providers often find overlapping software for CRM, reporting, transaction processing, etc. Simply running them in parallel squanders synergy; the value lies in harmonising into a cohesive architecture. Yet this is easier said than done – full IT integration is difficult, and some acquirers shy away from it. A notable example was BNP Paribas’s acquisition of Fortis, where the bank deliberately avoided fully merging IT systems, underscoring the perceived difficulty of “harmonising disparate systems.”[14]. Such avoidance may reduce short-term risk, but it also leaves potential synergies on the table. By contrast, look at UBS’s 2023 rescue takeover of Credit Suisse: UBS pursued aggressive systems integration, decommissioning 700 legacy applications from Credit Suisse in under two years, which helped it realise $9.1 billion in cost synergies by 2025[15]. This rapid consolidation of technology and operations – migrating 90% of Credit Suisse accounts onto UBS platforms within a year – put UBS well ahead of schedule at achieving about 70% of its $13B synergy target[16]. The UBS case illustrates that integration of IT and operations can directly drive EBITDA (through massive cost savings), albeit requiring upfront investment and diligent execution. It’s also a reminder that post-merger integration isn’t a one-time task; as UBS’s management noted, sustaining those synergies long-term will depend on continued technological modernisation (e.g. cloud migration, AI tools) fully integrated into the combined entity’s workflows[17].

Process & Workflow Integration: Beyond IT systems, aligning business processes is vital. Each firm comes into a merger with its own ways of doing things – how they onboard clients, how advisors make portfolio decisions, how compliance checks are done, etc. Post-merger, these workflows must be integrated or standardised to achieve efficiency gains. For instance, a trust services provider that acquires a competitor might integrate and streamline their entity administration processes, eliminating duplicate steps and harmonising to best practices. Done well, this can significantly reduce cycle times and error rates (as evidenced by the earlier stat of 30–40% reduction in order-to-cash cycle time with digital process integration[10]). Moreover, reengineering processes often uncovers opportunities for automation – e.g. using robotic process automation or AI to handle repetitive tasks like data entry, KYC verification, or report generation. Such automation not only cuts labor costs (boosting EBITDA) but also improves scalability. However, integrating processes requires careful change management. It may involve choosing one company’s process over the other’s or inventing a new approach altogether – and ensuring all employees adopt it.

People & Cultural Integration: Finally, the human element – integrating teams and cultures – is a cornerstone of post-merger success. Trust and wealth management are relationship-driven businesses; retaining top talent (advisors, fiduciary experts, client service staff) and getting them to collaborate in the new organisation is critical to prevent value leakage (like client defections or loss of know-how). Merged companies often face culture clashes or “us vs. them” dynamics that can impede synergy realisation. A well-integrated digital workflow can actually help unite people – for example, a unified CRM and communication platform encourages teams from both sides to work together servicing the same clients. But leadership must also actively manage cultural integration: setting common goals, aligning incentive systems, and investing in training so that employees feel comfortable with new systems and processes. According to PwC, 85% of executives report difficulty updating operating models and workforce habits to support new digital ways of working[18]. This highlights the importance of change management – employees need to see the benefits of new tools and be trained to use them, otherwise fancy technology investments may go underutilised. In summary, true post-merger integration spans technology, processes, and people. When all three are addressed in concert, the organisation is positioned to unlock the full EBITDA uplift promised by the deal.

The ROI of post-merger digital initiatives can be striking, especially when contrasted with more traditional integration moves. To crystallise the impact on EBITDA, consider some quantitative benchmarks from recent studies and cases:

Faster Synergy Realisation: Companies that prioritise digital integration see markedly faster financial improvements. McKinsey’s research shows a “digital integration premium” – those with high digital integration excellence hit synergy break-even 40% faster than peers[6]. Early synergy means a quicker positive impact on EBITDA (important for impatient investors). In practical terms, swift integration of IT and data can start yielding cost savings in months, whereas revenue gains from, say, new market expansion might take years. It’s telling that in 90% of successful deals, management had a clear value creation thesis early and invested in integration initiatives accordingly[19], often with a focus on tech-enabled efficiencies.

Faster Synergy Realisation: Companies that prioritise digital integration see markedly faster financial improvements. McKinsey’s research shows a “digital integration premium” – those with high digital integration excellence hit synergy break-even 40% faster than peers[6]. Early synergy means a quicker positive impact on EBITDA (important for impatient investors). In practical terms, swift integration of IT and data can start yielding cost savings in months, whereas revenue gains from, say, new market expansion might take years. It’s telling that in 90% of successful deals, management had a clear value creation thesis early and invested in integration initiatives accordingly[19], often with a focus on tech-enabled efficiencies. Improved EBITDA Margins: Digital transformation post-M&A tends to improve the efficiency (and thus profitability) of the combined entity. For example, after a comprehensive digital integration, a wealth manager might see its cost-to-income ratio improve as duplicative functions are eliminated. A global survey of wealth management deals found that those acquirers who effectively leveraged acquisitions to improve onshore operating efficiency did see profitability gains, whereas many who simply added scale without integration did not[23]. In private equity terms, investing in digital value creation can expand EBITDA multiples at exit; firms that lead with technology command higher valuations – one analysis noted they traded at ~8.2× EBITDA versus ~6.6× for less tech-enabled peers[24] (reflecting investors’ expectation of better growth and margins). Moreover, internal data from Strategy& indicates a successful digital overhaul can add hundreds of millions in EBITDA – e.g. a global oil & gas company achieved a $200 million EBITDA increase by redesigning its operating model and layering in digital tools post-merger[25]. While that example is outside our sectors, the principle holds: digitisation drives tangible financial outcomes.

Improved EBITDA Margins: Digital transformation post-M&A tends to improve the efficiency (and thus profitability) of the combined entity. For example, after a comprehensive digital integration, a wealth manager might see its cost-to-income ratio improve as duplicative functions are eliminated. A global survey of wealth management deals found that those acquirers who effectively leveraged acquisitions to improve onshore operating efficiency did see profitability gains, whereas many who simply added scale without integration did not[23]. In private equity terms, investing in digital value creation can expand EBITDA multiples at exit; firms that lead with technology command higher valuations – one analysis noted they traded at ~8.2× EBITDA versus ~6.6× for less tech-enabled peers[24] (reflecting investors’ expectation of better growth and margins). Moreover, internal data from Strategy& indicates a successful digital overhaul can add hundreds of millions in EBITDA – e.g. a global oil & gas company achieved a $200 million EBITDA increase by redesigning its operating model and layering in digital tools post-merger[25]. While that example is outside our sectors, the principle holds: digitisation drives tangible financial outcomes.In the TCSP and wealth management arenas, post-merger digital transformation has proven to be a high-ROI strategy, often outpacing traditional expansion or diversification efforts in driving EBITDA improvement. Digital integration addresses the fundamental challenge and opportunity of M&A: how to make two companies operate as one – more efficiently and profitably than before. By unifying systems, data, and workflows, and equipping the combined organisation with advanced technologies (automation, AI, analytics), acquirers can extract larger cost savings and enable revenue growth that directly boost the bottom line[10][5]. In contrast, strategies like entering new markets or adding product lines, while important for long-term growth, typically yield slower returns and depend on many external factors. They should be pursued, but not at the expense of neglecting the core integration. Indeed, many underwhelming M&A outcomes in wealth management can be traced to superficial integration – firms that simply added AUM or offices without streamlining operations saw little improvement in profitability[1].

For shareholders and investors, the message is clear: prioritise post-merger integration investments that modernise and unify the business. Encourage management to allocate merger budgets toward IT system consolidation, process automation, and data harmonisation early in the integration process. Insist on clear KPIs linking tech investments to EBITDA – for example, target a reduction in operating expense ratio, or track the increase in revenue per advisor after a new integrated CRM is rolled out. It’s also wise to maintain realistic expectations for revenue synergies from expansion plays; analysts tend to discount those, whereas realised cost synergies will be rewarded in valuations[22].

In practical terms, a balanced post-merger plan might look like this: achieve the “hard” synergies via digital-driven efficiencies first (to shore up EBITDA and fund further initiatives), while concurrently laying the groundwork to capture “soft” synergies like cross-selling through a unified client platform. Leverage the integration period to embed a digital mindset in the new organisation – for instance, standardise on a common workflow system and train all staff on it, so that the combined firm operates seamlessly. Also, use the momentum of the deal to rethink legacy practices: it’s an opportunity to re-imagine the operating model with technology at the centre, rather than simply bolt one company onto another. As one Deloitte report noted, modern dealmakers increasingly hinge their thesis on a target’s digital potential, not just its standalone EBITDA[29]. This reflects a recognition that in today’s market, digital maturity can multiply merger value.

Finally, consider real-world context: The global wealth and asset management report by Oliver Wyman and Morgan Stanley projects 20% fewer firms by 2029 due to consolidation, and those who thrive will be the ones that harness scale efficiently[30]. Efficiency comes from integration – of systems, processes, and people. For TCSP providers under the watch of private equity owners, it’s the same story: the playbook for improving margins and growing EBITDA is centred on automating compliance-heavy processes and integrating platforms across jurisdictions. In essence, digital transformation is the new synergy – it’s what turns the promise of a merger into tangible profits. Shareholders should champion this agenda, ensuring that post-merger value creation plans are not stuck in the 20th-century approach of just cutting headcount or opening offices, but are fit for the digital age of financial services.

Sources: Consulting reports and studies by McKinsey, BCG, Bain, Oliver Wyman, Deloitte, and PwC; academic research in Long Range Planning[13]; and industry case analyses (e.g. UBS-Credit Suisse integration) have informed the above insights, as cited throughout. All evidence points to a convergent conclusion – in post-merger scenarios today, integrating technology and operations is the surest path to EBITDA enhancement, providing a more controllable and often larger return on investment than traditional growth strategies[5][12].

[1] [2] [23] [30] Mergers & Acquisitions Trends In Wealth And Asset Management

[3] [4] [5] [6] [7] [8] [9] [10] [28] Buy-and-Build: Digital Synergy Levers for Maximum ROI in Corporate Acquisitions 2025 – Brixon Group

[11] Hg-and EQT-backed Quantios in add-on deal; Solar energy attracts private equity amid geopolitical tensions | PE Hub

[12] [20] [22] Eight basics for capturing deal value in mergers | McKinsey

[13] Brunel University Research Archive: Operating synergy and post-acquisition integration in corporate acquisitions: A resource reconfiguration perspective

https://bura.brunel.ac.uk/handle/2438/28435

[14] [15] [16] [17] UBS’s $9.1 Billion Cost Synergies: A Blueprint for Post-Crisis Megabank Consolidations?

[18] [25] Measurable digital value transformation outcomes: PwC

[19] [21] Why Some Merging Companies Become Synergy Overachievers | Bain & Company

https://www.bain.com/insights/why-some-merging-companies-become-synergy-overachievers/

[24] AI-Driven Personalisation in Wealth Management | nasscom

https://community.nasscom.in/communities/ai/ai-driven-personalisation-wealth-management

[26] [27] Asset and wealth management revolution 2024 | PwC

https://www.pwc.com/gx/en/issues/transformation/asset-and-wealth-management-revolution.html

[29] Private Equity–Driven Digital Transformation: Market Trends, Investments, and Strategic Shifts for 2025

Photo by Redd Francisco on Unsplash